Learn More

Economics

Weekly Economic Report: The Effect of TABOR on Government Revenue

by Wyoming Liberty Group Staff

The last Weekly Economic Report explained that there had been no visible effect on government spending in Colorado since the introduction of TABOR. This Report looks at the revenue side of the budget.

Main finding: The introduction of TABOR has had a limited but statistically visible effect on state revenue in line with what is expectable. It has also affected the state's revenue structure contrary to what is expectable.

In an effort to assess the potential for a Taxpayers Bill of Rights (TABOR) in Wyoming, the last Weekly Economic Report reviewed the effects of TABOR on government spending in Colorado. The conclusion was negative: no such effect was to be found. This Report turns to the revenue side, where TABOR appears to have left a footprint.

As explained in a separate article, there are some tests to be made on the revenue side in order to assess the relevance of TABOR. These tests focus on growth in state revenue and on the relationship between state and local government revenue. The hypothesis behind the second test is that the state would shift spending authority, and jurisdiction over revenue, to local governments, since they are not subject to TABOR.

A third test on the revenue side looks at the tax share of total state revenue; it is reasonable to expect that TABOR should reduce that share, since it exempts non-tax revenue.

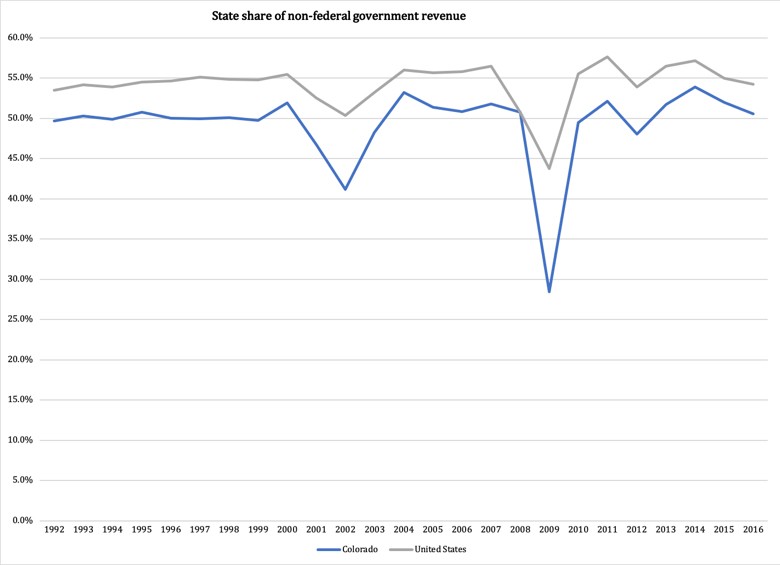

Figure 1 addresses the question of whether the state of Colorado has shifted revenue jurisdiction to local governments. From a statistical viewpoint, this does not seem to be the case:

Figure 1

Source: Census Bureau

Available fiscal data shows a small effect from TABOR on the state's share of revenue. While in the rest of the United States the state share has increased, the Colorado share remained flat throughout the first decade with TABOR. It is reasonable to expect this under a measure that makes it more difficult to raise taxes.

Beyond the first TABOR decade, the measure has not had any noticeable effect on state revenue.

Figure 2 breaks down state revenue per capita. Since TABOR has a per-capita feature for controlling revenue growth, it is reasonable to expect a noticeable difference between per-capita state revenue growth in Colorado vs. the country as a whole. However, if Colorado has experienced a significantly different demographic development than the rest of the country, we could expect a different result than in Figure 1.

That is not the case:

Figure 2

Source: Census Bureau

The TABOR effect from Figure 1 is slightly more pronounced in Figure 2. The effect is not strong, as the fluctuations in Colorado state revenue follow the national pattern. However, the gap between per-capita state revenue in the Centennial State and the United States as a whole is sustained and widens moderately over time.

The data reported in Figures 1 and 2 thus speak in favor of TABOR, a conclusion to be weighed against the fact that there is no visible effect on the spending side.

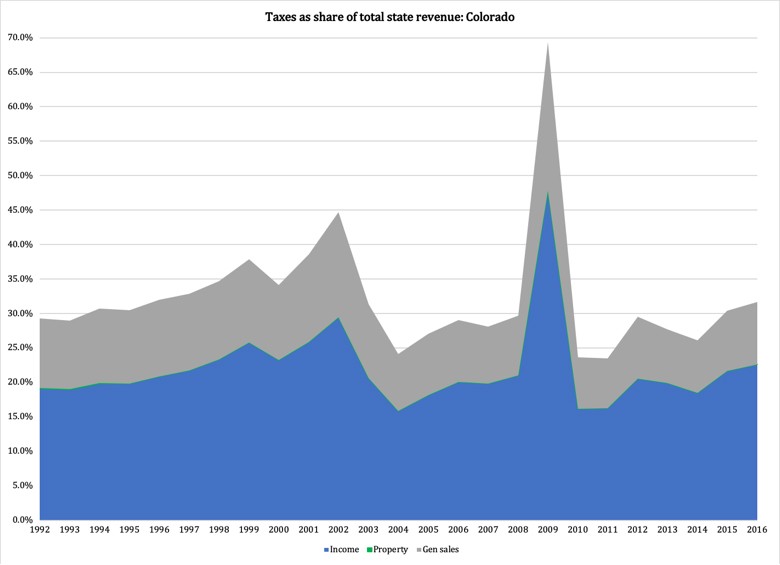

Figures 3 and 4 report data on the tax share of total state revenue. The tax share is measured as the sum total of corporate and individual income taxes, general sales taxes and property taxes, which is then divided by total revenue.

According to Figure 3, these taxes were responsible for a higher share of state revenue in 1999 than they were in 1992, the year TABOR was passed. The year 1999 is relevant because it marked the peak of the 1990s growth cycle. Therefore, the revenue structure in place performed at its strongest at that point, thus allowing for the best possible comparison to the pre-TABOR revenue structure:

Figure 3

Source: Census Bureau

The income, property and general sales tax share of total state revenue in Colorado rose from 29.3 percent in 1992 to 37.9 percent in 1999. It is not immediately clear why this happened; the a priori expectation would be the opposite.

A possible explanation is strong GDP growth that benefited tax revenue over non-tax revenue. A separate test will control for this effect.

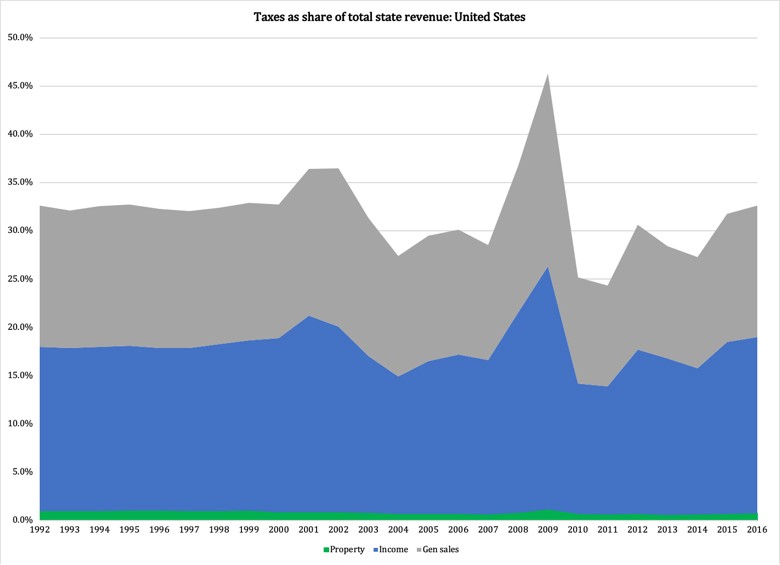

For comparison, the aggregate state-revenue data for the United States are reported in Figure 4:

Figure 4

Source: Census Bureau

Beyond approximately the first decade with TABOR, Colorado does not stand out particularly when it comes to the tax structure. The peak in 2009, which is associated with the rapid rise in unemployment and rapid decline in revenue for government pension funds, is an anomaly that the Centennial State shares with the rest of the country.

In conclusion: there are some positive effects of TABOR visible in state revenue data. These effects are not strong enough to outweigh the lack of visible influence on government spending, but they do merit further inquiry into the matter.

The only remaining revenue-side question regarding TABOR is whether or not the rise in the tax share of total state revenue is attributable to GDP growth. That question will be answered in a future Report.

![]()

Wyoming Liberty Group

P.O. Box 9 • Burns, WY 82053

Phone: (307) 632-7020